In an earlier article, we looked at the trends in financial planning that are already in use and which ones companies want to adopt in future. In this article, we examine how best-in-class organizations differ from laggards in their approaches to financial planning.

Which of the following does your company do/use with your product for planning and budgeting? Best-in-Class vs. laggards, (n=125)

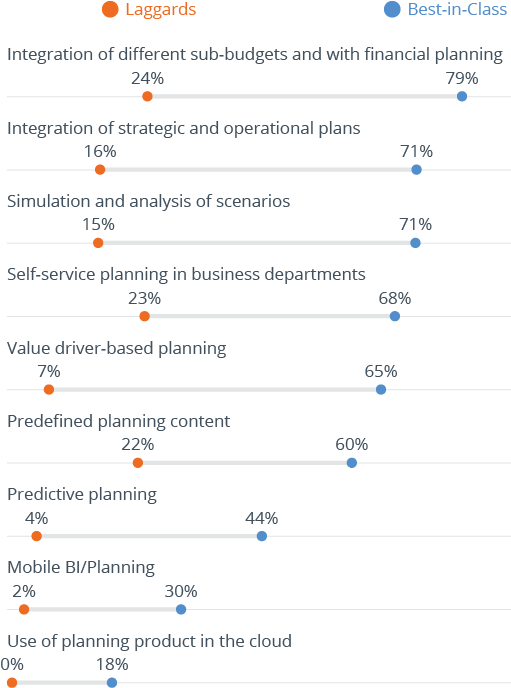

A comparison between best-in-class enterprises and laggards shows that best-in-class companies are more open to trending topics. In particular, their higher level of planning maturity and more solid grasp of the planning basics puts them in a better position to address advanced planning topics and benefit from their advantages.

Some examples of these subjects include:

- Better integration of strategic and operational plans, as well as of different sub-budgets with financial results planning, lead in many cases to a significantly higher quality of planning results.

- In a volatile economic environment, companies have to react to changes quickly. Simulation and the analysis of scenarios (best case/worst case) provide companies with the ability to replace their ‘best guess’ with objective assessment criteria to minimize the risk of making bad decisions.

- Predictive analytics and prognosis are major trends in the market that also affect planning (‘predictive planning’). In particular, the automation of forecasting processes with consolidated estimates using statistical predictions offers the possibility for companies to shorten or automate at least parts of their planning processes.

BARC speaks with many companies and the main problem they often face when addressing trending topics is a lack of expertise. This applies in particular to laggard companies where essential planning basics are often absent, or planning is only established at a very rudimentary level. In these organizations, expertise on the topic and experience of how to proceed are the main limiting factors.

For further insights see The Planning Survey 16.